Who is afraid of Grey, Green and Red: A story of three zones

PFZW [Pension Fund for the Health and Social Sector] and its administrator PGGM, are among the most progressive sustainable and responsible investors among pension funds worldwide. Yet, in the view of, for example, participants, NGOs, and sometimes politicians, we are doing far too little in this area. Seen from their perspective, that is an understandable reaction, but we also have to draw a line.

The reason for this is simple enough. As a pension investor, we serve the interests of our participants, who deposit a premium in exchange for a pension. To a high degree this is a financial interest on the part of individual participants. By contrast, sustainability primarily is a social good and a collective interest.

These two aspects can reinforce each other, but they can also be in conflict with each other. It is important to note that the optimal policy for the participants in pension funds is not the optimal policy for society as a whole, and vice versa.

This brief note provides a simple framework that clearly outlines these interests. When we agree on a framework, this enables us to conceive of measures designed to enlarge the zone in which pension funds act in the interest of their participants, as well as in the interest of society as a whole. We refer to this zone as the green zone.

Current approach to investing by pension funds

The neoclassical economic theory over the past few decades has had a tremendous influence on the thinking and actions of almost all financial institutions and companies. The same applies to pension funds as investment institutions. This has resulted in major progress in the area of investing, but has also resulted in a number of drawbacks.

Two elements are of importance here: 1) the reduction of investing to an activity that can be described purely in terms of risk and return – to paraphrase Milton Friedman: the business of pension funds is generating returns. 2) the stubborn idea that there is a single universal 'optimal' portfolio, that every deviation from this is a 'risk', and that investors therefore are prepared, or rather are virtually obliged, to purchase all available investments on the market – at any price.

These two elements to a high degree have reduced investing to an engineering problem. In this context, having regard for the social consequences of investments, for example in the form of climate change or contributing to the broader prosperity of a society, virtually by definition is a deviation from the fiduciary task and the interest of participants. And, for that matter, this is how many investors perceive this as well.

Society's demand

This approach is far removed from what society is demanding increasingly more emphatically and explicitly from pension investors. Society is asking pension funds and investors what they will be contributing to the sustainable development of the world we live in. How is the enormous capital we have entrusted to you going to have a real impact, so that the world starts moving in the right direction: away from untenable activities (climate change, pollution, destruction of biodiversity) towards making a visible contribution to sustainable prosperity and welfare?

Or more fundamentally: is the financial return you are harvesting being offset by excessively high costs that burden society as a whole? Are you making a sufficient contribution to society?

Combining financial and social returns

With the rapidly increasing priority of sustainability on the social agenda, the challenge is having investors and pension funds materially contribute to the realisation of the desired impact and change.

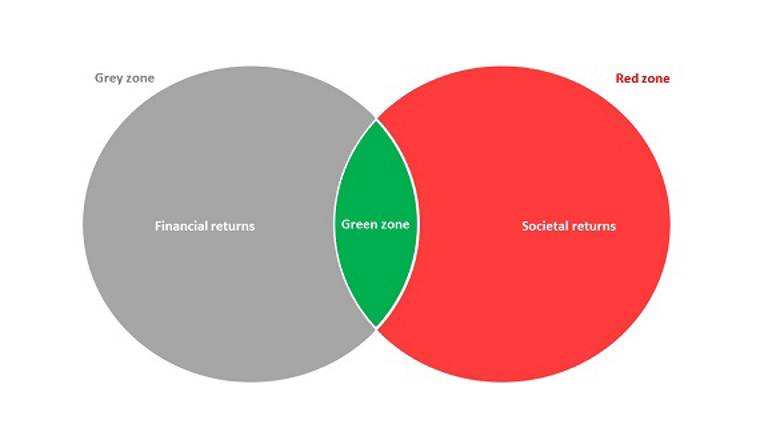

To stimulate thinking on this subject, we are introducing a framework that comprises 3 zones:

- the grey zone in which investors are solely focused on the financial dimension of their investments – the individual participant wins, the social costs are passed on to the collective.

- the green zone which integrates sustainability to the maximum possible extent without sacrificing financial goals – the participant, as well as society wins.

- the red zone in which the focus on society's goals is such that this is at the expense of the individual participants in the pension fund – the participant subsidises society.

Two conclusions are immediately evident from this framework: (1) you are not going to change the world for the better in the grey zone and you do not consider this to be consistent with your task; and (2) as a pension fund, you do not want to end up in the red zone – although the collective interests are served, you harm the individual financial interest of your participants. Without pressure, investors will not enter the red zone, unless they have an express mandate from their participants for this purpose.

This is why, in my view, the key question is: how can we enlarge the size of the green zone, so that both the participant's interest and society's interests can be better served than is currently the case?

The diagram illustrates the 3 zones:

- The grey zone is large: the bulk of the pension fund's capital is invested here. This may be paired with major social costs that are not priced in. The object here is to maximise the return per unit of risk.

- The red zone is large as well: this is the zone in which society could become sustainable, but which is beyond the reach of investors, because this zone is at the expense of the return/risk ratio.

- The green zone is relatively small. The objective here is to maximise the contribution to sustainability without doing so at the expense of the return/risk ratio.

How to enlarge the green zone

The green zone can be enlarged by reducing both the grey zone and the red zone.

In my view, a great deal can be achieved here on the pension fund and investor side.

First, it helps if participants explicitly identify the importance they attach to sustainability.

Second, it is also important to have proof and examples of positive impact that is not at the expense of financial return, but can even contribute to it. This proof is increasingly available.

Third, it would help if investors and pension funds would take a longer-term horizon into consideration over which to evaluate their investment decisions. Over a horizon of one year there is not a great deal that can be said about the impact of climate change on companies that operate in the oil sector, but over a horizon of ten years a great deal more can be concluded.

Fourth, it would help if we were to let go of the neoclassical dogma and embrace the idea that there is not one optimal portfolio, but that there are many different sensible portfolios.

A great deal can also be achieved on the social and government side, and a great deal is already happening here. In the first place, it is important that society considers pension funds from a stakeholder perspective: you do not earn your place as an institute by fully focusing on the participant as the stakeholder, without considering the social consequences.

Furthermore, consistency and clarity concerning the long-term policy objectives is a very powerful tool. For example, the Paris agreements, clear policy objectives and a clear path towards carbon pricing make it possible for investors to tangibly identify the long-term risks and to translate them into strategic decisions relating to the allocation of their capital.

More generally: a government that clearly indicates that there are undesirable externalities and that develops policy focused on pricing these externalities, operates as a powerful catalyst. Governments will have to work together on an international scale to ensure the creation of a level playing field.

Conclusion

By adopting the grey-green-red framework, it becomes clearer why pension fund investments are not always as green as society might like. Using the framework as a basis for thought development helps create insight into a toolkit that we can use to enlarge the green zone. Pointing fingers is useless in this regard. Filling the toolkit is a joint task for pension funds and policymakers. This is in everyone's interest.

Share or Print Article

click on the icon