Collateralisation

For that reason, we always ensure that the full notional of our transactions is invested such that we are not exposed to unsecured credit risk of the risk sharing bank. Collateralisation of the investment notional is engrained in our mandate.

We will start with describing why we believe that collateralisation of the investment notional in a CRS transaction is important from the perspective of an investor. This will include a description of the structures via which this can be implemented and why we believe collateralisation is superior to two common alternatives to alleviate counterparty risk in CRS transactions. Further, we will describe the benefits of collateralisation for banks and from a supervisory perspective as well.

Investor Perspective

A CRS transaction is an attractive way for investors to get access to unique credit exposures that are not easily available in public markets and to partner with banks in the lending businesses that they know best. We believe that a CRS transaction should be structured to simply achieve this element alone: exposure to the credit risk arising from the lender’s management of the underlying loan portfolio. It should not come with any other risks to the lender and certainly not bank default risk.

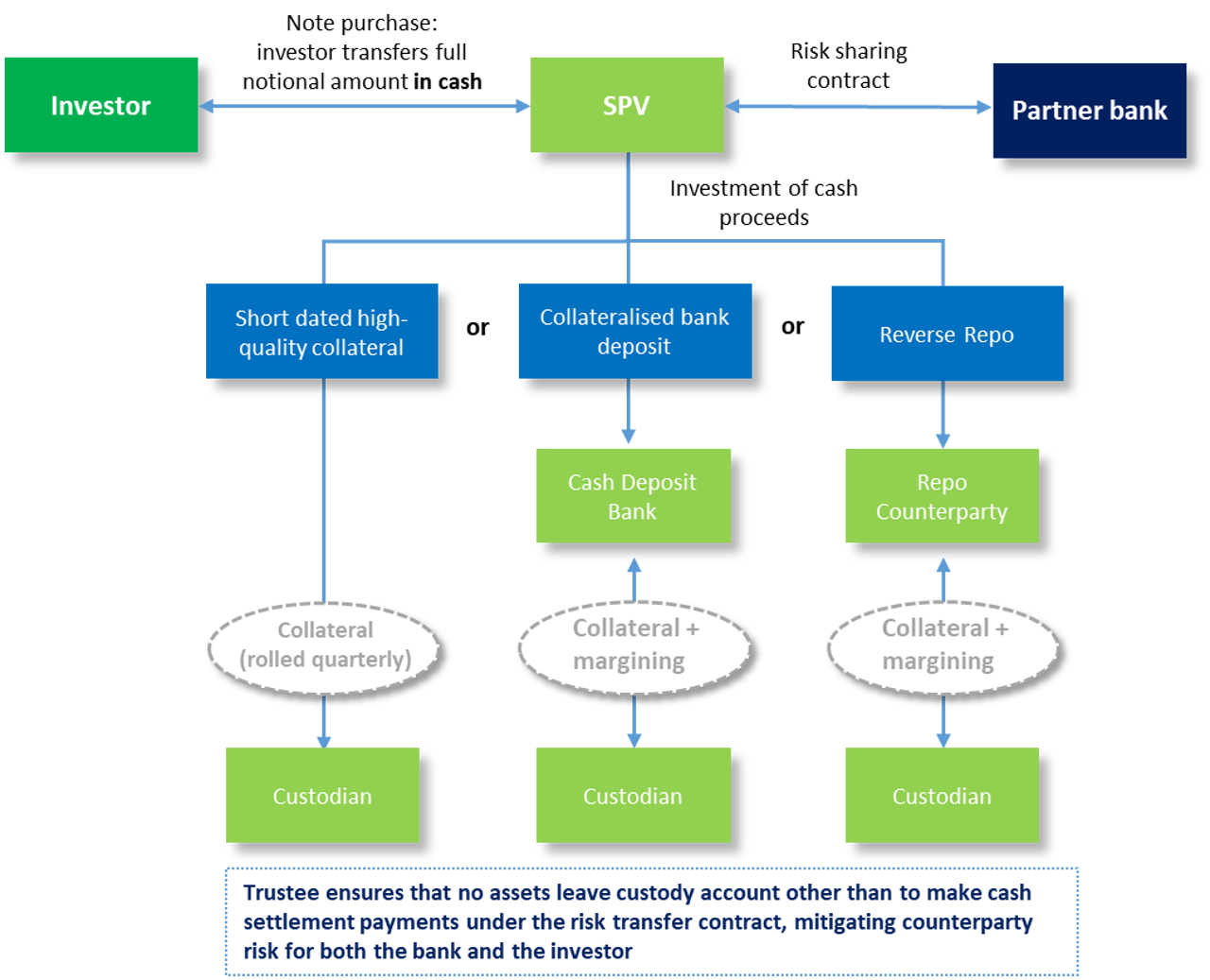

In our transactions we always ensure that the full notional of our transactions is invested such that we are not exposed to unsecured credit risk of the risk sharing bank. At the same time, there is always certainty of funds available to the bank when a valid credit event claim needs to be paid. To achieve this, we have adopted quite straightforward structures: either the bank collateralises the investment notional by providing high-quality collateral (via a collateralised bank deposit or a reverse repo) or the investment notional is directly invested in high-quality short-dated collateral. These ways of collateralisation have been accepted by all our counterparties for many years. Another alternative could be to invest the investment notional in a money market fund, a structure that has become commonplace in, for example, the cat bond market since the default of Lehman. In any of these cases, the transaction is structured such that collateral cannot leave the transaction and can only be used to fulfil any cash settlement payment obligations under the risk sharing contract as they arise. This ensures that neither the investor nor the bank runs counterparty credit risk vis-à-vis each other. For the avoidance of doubt: the investor bears the risk and return of the underlying collateral.

A key benefit of this collateralisation approach is that investors can also be there in more challenging times, when the future of the bank looks uncertain and is challenged by the market. As long as investors are comfortable that the underlying lending business continues to be run in a business-as-usual fashion, under existing or new ownership, the continuation of the credit hedge is acceptable.

This is not just true in theory. Since the inception of our mandate in 2006, we have closed transactions every year. Throughout this period there have been multiple moments where one or more banks faced elevated funding and capital costs, in the aftermath of the global financial crisis and occasionally thereafter. Separating the credit risk of their core lending books from the heightened counterparty risk of the bank has enabled us to continue doing transactions in these circumstances at a fair price, leaving the cost of increased counterparty risk out of the equation.

Alternatives to collateralisation

We believe that collateralisation is superior to two common alternatives that are employed to reduce the credit risk to a risk sharing bank: (i) implementing rating downgrade triggers and (ii) hedging the counterparty risk in public markets.

In some CRS transactions with an unsecured cash deposit at the risk sharing bank, rating downgrade triggers are put in place. These stipulate a transfer of the cash deposit to another qualifying bank in case the partner bank experiences a severe rating downgrade. Unfortunately, first-hand experience shows that these rating triggers do not work well: the transfer can be operationally cumbersome and take a long time, at least several months and sometimes even more than twelve months. It is a time consuming challenge to find a suitable and willing new counterparty and to execute such a transfer. This can be particularly difficult in times of market distress, when many other such transactions, and many other banks are in the same position. For the bank this would mean a loss of funding after a credit downgrade, further worsening its credit position.

Another alternative to collateralisation is to try and hedge the counterparty risk to the bank through credit default swaps in the public market. This is currently done by some investors in the market, especially when they do not have the negotiating power to require the bank to collateralise within the transaction structure. While this provides some mitigation of bank counterparty risk, the ability to use public CDS depends on the size and liquidity of the market. With increased issuance and wider first loss tranches leading to larger absolute investment amounts, it becomes increasingly difficult to find sufficient liquidity in the CDS market. Furthermore, even if there would be sufficient supply and liquidity, there will be basis risk as it is impossible to find a credit default swap that perfectly matches the counterparty risk. Firstly, the events under which a public market CDS is triggered might not perfectly match the counterparty risk the investor faces through an uncollateralised synthetic securitisation. Secondly, the notional of CRS transaction can amortise more or less quickly than expected, due to losses or prepayments, leading an investor to have to adjust the tenor of its hedge and incur market risk by buying or selling CDS in the public market. Lastly, CRS transactions typically include call rights for the bank (such as time call, clean-up call or regulatory call), which exacerbates the problem. Again, particularly in times of market distress, such issues become even more difficult to manage.

Bank perspective

For a bank, the main rationale for entering into a CRS transaction is for capital or risk management purposes. Keeping the cash notional of a CRS transaction may have some (term) funding benefits for the bank, but due to the first loss nature of the transaction, the absolute funding amount is relatively small and the term is not certain. Therefore, if funding is the bank’s primary objective, then it has many other and far more efficient tools at its disposal to achieve this, such as issuing a true sale securitisation and selling the senior tranche.

Choosing against putting the cash notional on an unsecured deposit can have a benefit for the risk sharing bank that is sometimes overlooked. If the bank has taken the cash notional as unsecured funding, then a bank default automatically triggers a termination event under the risk transfer contract, leaving the bank without a credit hedge at a time when it is most needed. In case of a collateralised structure, if the bank were to default while the bank’s estate continues to pay the coupon for the credit hedge, the protection can remain in place. Especially when the credit hedge is on a core lending activity that has a reason to exist, that lending business itself will have value in a workout or restructuring situation. That is a sound basis to assume the business will continue to have the resources needed to run as usual, not necessarily affecting the credit risks shared with investors.

Collateralising the investment notional also provides the bank with more execution certainty in times of distress, as it is less dependent on the willingness of investors to accept its counterparty credit risk and the likely elevated costs in such scenario. As mentioned before, our first-hand experience demonstrates this well.

Supervisory perspective

As mentioned above, in case the investment notional is uncollateralised, the bank would typically use this as funding in its general operations. This creates a complication in case of a bank default. The bank accounts for the cash notional as funding, being able to use it as it pleases, while also assuming it is available to cover loss claims when they arise. At the moment a bank defaults, there is no dedicated collateral to cover credit protection claims, as the cash collateral meant to cover these has already defaulted along with the rest of the bank. Consequently, the transaction would need to terminate and the credit protection on the bank’s loan portfolio ends. As a result, the risk weighted assets of the bank immediately flow back to the balance sheet, further worsening the capital position of the bank at the worst possible time. On top of that, there is a claim from the investor on the funding provided.

The importance of counterparty credit risk has been one of the key lessons of the global financial crisis of 2008. Since then, there has been a clear regulatory drive towards limiting counterparty risk, for example the move towards central clearing for derivatives, and more generally towards increasing transparency about the risks involved in a transaction. We believe collateralisation fits perfectly into this trend, because mitigating counterparty risk for both sides ensures the transaction performance is purely driven by the credit risk of the underlying loan portfolio.

Comparison to true sale securitisation

Both a true sale securitisation and a synthetic securitisation are investments in credit risks originated by banks. By its nature, a true sale securitisation is collateralised by the underlying loans as these have been sold to the SPV. Therefore, an investor in a true sale securitisation does not run counterparty risk to the originating bank. The underlying loans in a synthetic securitisation are not transferred to an SPV, but remain on the balance sheet of the bank. This means that collateralisation of the investment notional is required to arrive at the same position in terms of bank counterparty risk as in a true sale securitisation.

The below graphic clarifies this point by comparing the situation before and after a bank insolvency for 1) a true sale securitisation, 2) a funded and collateralised synthetic securitisation, and 3) a synthetic securitisation where the funding is put on deposit with the bank. It highlights that a synthetic securitisation can achieve an equal level of protection for bank and investor in terms of counterparty risk compared to a true sale securitisation, but only if the transaction is funded by the investor with cash and if that funding is collateralised, thereby remaining fully separated from the default risk of the bank.